In the last 2 decades, we have seen how technology has significantly changed how we make payments globally. We’re rapidly moving from a cash-focused global economy to a cashless one. While cash is still king in most developing countries, businesses and consumers are swiftly embracing digital payments in those countries.

One of the leading digital payment options we have is Cards. Almost everyone who is financially included has a credit or debit card they can use to complete online payments.

In our increasingly digital world, the convenience of online card payments is something we often take for granted. We click “Pay Now”, expecting a smooth payment process and instant confirmation. But then, the dreaded message appears: “Your payment has been declined”. This is a frustrating experience, whether you’re a customer trying to make a purchase or a business relying on seamless transactions.

Understanding why these failures happen is the first step to minimizing their occurrence and impact. In this article, we’ll delve into the common reasons why your card payment might not go through. We’ll group these common reasons into similar buckets to make them easy to understand.

Card Details and Account Status

These are often the simplest issues to resolve, yet they are quite common:

- Incorrect Information: A simple typo in the card number, expiry date, or the CVV (Card Verification Value) is an immediate red flag for the payment system. It’s important to always confirm these details when making a payment.

- Expired Card: All cards have a validity period. Attempting a transaction with an expired card will lead to a decline from the issuing bank.

- Card Reported Lost or Stolen: Once a cardholder reports their card as lost or stolen, the issuing bank immediately blocks it to prevent unauthorized use. Any transaction attempts thereafter will be rejected.

- Insufficient Funds: This is one of the most common reasons for declines, especially with debit cards. If the account balance doesn’t cover the transaction amount, the bank will not authorize it.

- Reached Credit or Spending Limits: Credit cards come with a specific credit limit. Exceeding this, or even a “shadow limit” that some card issuers use based on spending patterns (even on cards with “no pre-set spending limit”), will cause a decline. Many banks also apply daily or per-transaction spending limits for security.

Security Measures and Fraud Prevention

While sometimes inconvenient, many declines are the result of robust security systems designed to protect both cardholders and merchants from fraudulent activity. This is where the roles of card networks and payment gateways become critical:

- Address Verification System (AVS) Mismatch: AVS compares the billing address entered by the customer with the address on file at the issuing bank. A discrepancy can signal potential fraud and lead to a decline.

- Failed 3D Secure Authentication: 3D Secure is an extra layer of security that card networks use to prevent fraud; for example, Visa Secure, Mastercard Identity Check, Discover ProtectBuy, and American Express SafeKey. This usually involves the cardholder performing authentication via challenge by entering a one-time password (OTP) sent to their phone or email, or using biometric verification, or using a frictionless flow, which requires no biometrics. If this authentication step fails, the transaction will be declined to prevent unauthorized use.

- Suspicious Activity Flags: Issuing banks and card networks employ sophisticated algorithms to detect unusual transaction patterns. These might include:

- A purchase significantly larger than the cardholder’s typical spending.

- Multiple transactions in rapid succession.

- Transactions from a new or unexpected geographical location, especially if it’s a high-risk area.

- Use on a website that has been flagged for suspicious activity.

Banks & Systems

Sometimes, the reason for a decline is less about the cardholder or the specific transaction and more about the systems involved:

- “Do Not Honor” or Generic Decline: This is a common, yet opaque, response from the issuing bank. It essentially means the bank is not willing to authorize the transaction for reasons it doesn’t disclose. The cardholder would need to contact their bank directly for more information.

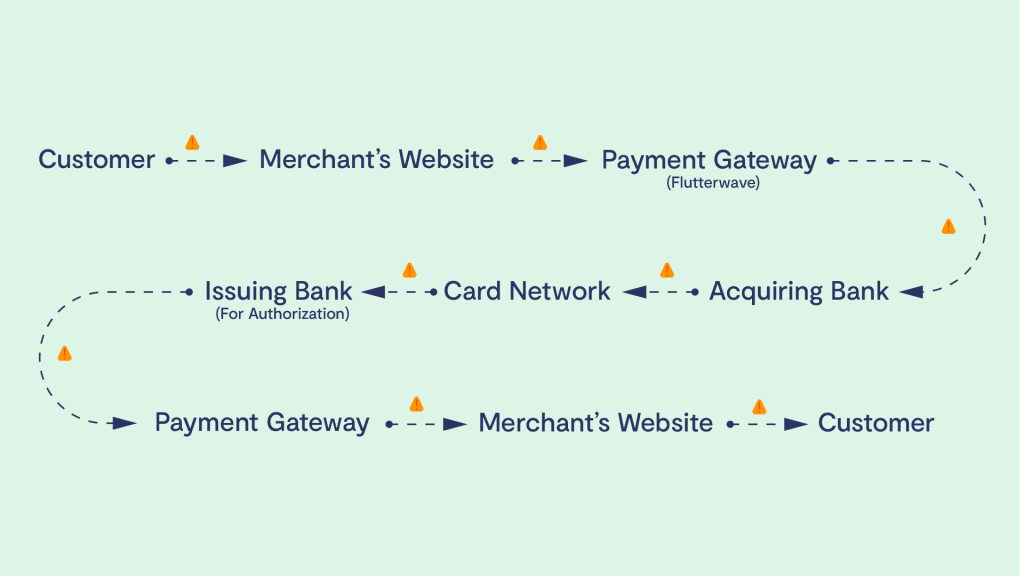

- Communication Errors or Timeouts: In the split second a transaction takes to be authorized, information travels between the merchant’s website, the payment gateway, the acquiring bank (the payment gateway’s bank), the card network, and finally, the issuing bank (the customer’s bank). A temporary glitch or timeout in communication at any link in this chain can cause the transaction to fail.

- System Downtime or Maintenance: Though service providers strive for constant uptime, any of the involved parties (banks, card networks, payment gateways) can occasionally experience technical issues or scheduled maintenance that may temporarily prevent transactions from being processed.

Merchant’s Integration and Acceptance

Although not so common, issues can also arise from the merchant’s end:

- Incorrect Gateway Setup: While payment gateways aim for simple integration, errors in how a merchant has configured their payment services can sometimes lead to failed payments. Our APIs are optimized for easy integration. Learn more in our documentation.

- Currency or Regional Mismatches: The merchant may not be set up to accept payments in certain currencies, or there might be cross-border restrictions imposed by their payment processor or bank.

- Card Type Not Supported: This occurs when the payment gateway can’t process payments from that particular card type. Flutterwave is consistently working to broaden our card network acceptance, which is why we’ve partnered with some of the biggest card networks in the world to enable seamless payment processing.

How Card Networks Protect Your Account

Card networks invest enormous resources in global fraud detection. They monitor transactions across their networks in real-time, looking for anomalies. They utilize advanced machine learning models and vast datasets to identify potentially fraudulent transactions, often intervening to protect the cardholder even before they realize their details might be compromised. This proactive security is vital, regardless of the payment gateway being used.

How Flutterwave Protects You & Your Customers

Payment gateways like Flutterwave play an active role in securing every card transaction. We have achieved PCI-DSS (Payment Card Industry Data Security Standard) Level 1 compliance – the highest global standard for data security in the payments industry. This means we adhere to stringent controls for handling cardholder data. Furthermore, we have our fraud detection tools, risk scoring engines, and support for 3D Secure v2, providing an additional layer of defense for merchants and peace of mind for customers. You can learn more about how Flutterwave protects you and your customers in this blog.

Moving Towards Smoother Transactions

Payment declines are an inherent part of the digital commerce landscape, often serving as a necessary checkpoint for security. While they can be frustrating, understanding the underlying reasons can help businesses reduce their frequency and enable customers to easily resolve them.

The payments industry, from card networks and issuing banks to payment gateways, is constantly innovating to enhance security while improving user experience. By implementing tough security protocols, leveraging AI for fraud detection, and ensuring robust communication channels, these players work collaboratively to make digital payments safer and more reliable for everyone.

So, while a “payment declined” message might still pop up occasionally, the systems behind the scenes are working hard to protect your financial information and ensure the integrity of every transaction.